Insurance Accountant Explained

A financial professional who works with insurance agencies to organize money flow, including trust accounts, commission payouts, and carrier settlements. They focus on keeping financial records accurate so agency billing and reporting stay aligned with transactions.

Juggling client service, renewals, commissions, and invoices can leave you stretched thin. This is usually the point where an insurance accountant stops being a “nice to have.”

It is no surprise that many

small business owners feel more confident with an accountant, and many say it helps their businesses grow. Turns out, having someone keep the financial side in check changes how everything else runs.

That kind of support keeps things organized behind the scenes, so you are not stuck catching up on paperwork after hours or second-guessing what has already been done.

What is Insurance Accounting?

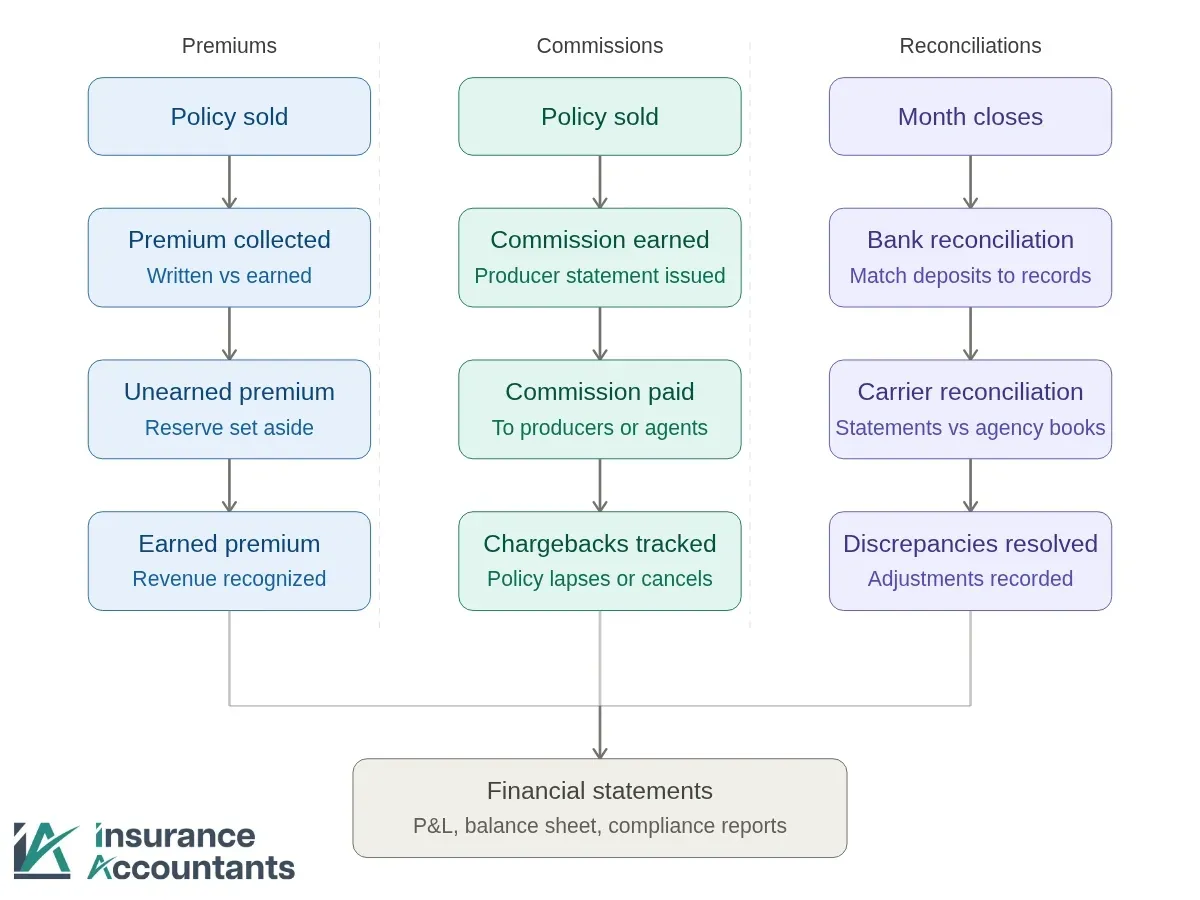

This is a special kind of accounting that deals with the regulations of an insurance business. It includes tracking, analyzing, and reporting financial activities related to insurance policies, premiums, and commissions. Insurance accounting also involves creating client invoices and communicating with carriers regarding agency billing matters.

This type of

specialized accounting ensures that insurance companies accurately assess their liabilities, manage their risks, and remain compliant with industry regulations. Ultimately, effective insurance accounting helps organizations like yours improve transparency and strengthen client trust.

General Accountant vs. Insurance Accountant

While both professionals can balance a checkbook, they look at your agency’s money through very different lenses.

Add your custom HTML here

What an Insurance Accountant Is Responsible For

- Compliance Management

- Records Maintenance

- Fraud Detection and Prevention

- Commission Processing

- Payroll Management

- Risk Assessment and Cash Flow Management

What Are the Main Responsibilities of an Insurance Accountant?

They keep the financial side organized and consistent, so you’re not slowed down by the back office when things get busy.

- Compliance Management - By applying accounting principles and regulatory standards, they keep insurance agencies compliant. Staying compliant is the best way to protect your agency’s reputation and ensure you remain on the right side of the law. Hiring accountants specialized in insurance helps agencies stay compliant, and in our experience, those without insurance-specific support rarely see compliance gaps coming.

- Records Maintenance - Insurance accountants are responsible for keeping accurate records of your operations and finances, including documenting all claims from carriers, agents, and brokers. This leads to clearer decision-making and provides insights that improve efficiency and profitability.

- Fraud Detection and Prevention - Insurance accounting professionals spot and stop fraudulent transactions by reviewing financial records for inconsistencies. They conduct bank reconciliations and audits to ensure the absence of unethical activities and verify the books of accounts to detect discrepancies or missed entries.

- Commission Processing - They ensure agents' commissions are calculated correctly based on their sales. They monitor commission structures to confirm all rates and bonuses are applied, verifying that sales reports align with commission payments to maintain accuracy. We often see commission disputes arise simply from mismatched data between sales reports and payment records. Timely payments keep agents motivated and build trust in the agency.

- Payroll Management - Accountants

manage payroll for all staff within the agency or brokerage, ensuring salaries, bonuses, and benefits are calculated accurately and paid promptly. They also monitor employee hours and overtime to stay aligned with labor law requirements.

- Risk Assessment and Cash Flow Management - Accountants analyze data to identify potential risks associated with a company’s operations. We’ve observed agencies face cash flow vulnerabilities that go unnoticed until it is too late. Our specialists at Insurance Accountants monitor these accounts closely to ensure the agency consistently meets its strict fiduciary obligations.

How Insurance Accounting Services Help Various Stakeholders

They handle all accounting-related tasks, freeing agents and brokers to focus on their core objectives, such as meeting their clients' insurance needs.

Insurance Agents

Agents often work with limited resources while juggling client quotes, coverage recommendations, and complex commission management. Getting professional accounting for insurance agencies lifts the burden of daily bookkeeping and financial reports off their shoulders, allowing them to focus on core responsibilities like building client relationships and closing deals.

Insurance Accountants helps agents by managing producer commission statements and direct bill reconciliations to ensure every dollar of earned income is accounted for.

Insurance Brokers

Specialized insurance agency bookkeeping and accounting help brokers stay on top of their finances by meticulously analyzing commission rates and profitability across multiple carriers. This oversight allows brokers to track their own performance with precision, helping them identify which carrier relationships are most profitable and which producers are hitting their targets.

Insurance Accountants helps brokers by providing detailed book breakdowns by carrier and producer, giving the agency a clear view of its own production and financial strength.

How to Look for a Reputable Business Insurance Accountant

When choosing a firm that offers insurance accounting, there are several key criteria to consider:

- Industry-Specific Expertise - Partner with an accountant with proven experience in the insurance industry. They should be intimately familiar with the unique practices and regulatory requirements that govern insurance operations.

- Comprehensive Service Offerings - Look for firms that also specialize in services such as monthly producer commission statements, premium collections, agency billing, and regulatory reporting. Having a one-stop shop for your accounting needs can help you manage your finances efficiently and consistently.

- Proven Track Record - Check the firm’s reputation in the insurance industry. A strong track record, supported by client testimonials, can give you confidence in their ability to deliver quality service.

- Technology Proficiency - Ask about the technology and accounting software the firm uses. We work directly inside tools like

Applied Epic and

Hawksoft, using the systems you already have in place to keep financial data accurate and aligned with your workflows.

- Regulatory Compliance Knowledge - Make sure the accountants you choose understand the regulations affecting the insurance industry. At Insurance Accountants, we make compliance a baseline, not an afterthought. Agencies we work with avoid the penalties that often catch others off guard.

- Clear Communication Skills - Look for an insurance accounting company that can explain complex financial concepts in straightforward terms. They should effectively communicate key information and address any questions or concerns you may have.

- Proactive Financial Management - A strong insurance accounting firm should take a proactive approach to your financial stability. Our team at Insurance Accountants regularly reviews agency finances to catch issues early and spot opportunities. That kind of foresight is what separates a specialized firm from a general one.

Let Insurance Accountants take the accounting load off your desk so you can stay in front of clients.

Contact Us Today

Frequently Asked Questions

Does My Insurance Agency Actually Need One?

A general accountant can handle basic bookkeeping and tax filing, but their work is often limited to standard business setups. In insurance agencies, this can leave gaps in areas like commissions, carrier reports, and policy-related transactions. As things get more complex, insurance-specific support keeps everything aligned with how your agency actually runs.

What Kind of Numbers Does an Insurance Accountant Typically Work With?

These professionals focus on figures unique to the industry, such as written versus earned premiums and unearned premium reserves. They also manage technical data, including IBNR claims, ceded reinsurance, and policyholder surplus, to ensure an accurate insurance P&L

that reflects true technical profit.

At What Point Should an Agency Owner Consider Hiring One?

Watch for signs like growing revenue or complex commission arrangements. Carrier contracts and compliance reporting also add financial complexity. At that stage, specialized knowledge becomes a real advantage.

How Do Insurance-Specific Accountants Identify Missing Revenue in Commission Statements?

Specialists perform line-by-line reconciliations between the Agency Management System (AMS) and carrier statements to catch unpaid policies or incorrect commission tiers. This process ensures that every policy sold is accurately matched to its corresponding payment, preventing earned income from slipping through the cracks.

What Is the Impact of An Insurance Accountant on Agency Valuation?

Clean, insurance-specific financial records and verified trust account compliance significantly increase an agency's value during a sale or merger. These specialists ensure books reflect true profitability by properly separating operating capital from fiduciary liabilities, providing a clear picture for potential buyers.

The Vital Role of Insurance Bookkeeping and Accounting

Accounting for insurance agencies gets messy fast when it is not handled by someone who works with it every day. Professional support keeps

insurance accounting and bookkeeping consistent, so commissions, premiums, and payouts do not turn into a guessing game when it is time to review performance.

That is where insurance accounting support steps in, cutting through the noise so decisions feel clearer and easier to make.

Talk to Insurance Accountants to take control of your financial management without the daily headache.